Which HEI Company Funds Fastest? 2026 Speed Comparison

Splitero is consistently the fastest home equity investment provider, with pre-approval often in one to two business days and funding in roughly two to three weeks. Hometap and Point typically fund in about three weeks, while Unlock runs longer at 30 to 60 days. Your actual timeline depends on your appraisal, your documentation, and how quickly you respond during the process.

The Scout Executive Summary

- Splitero leads on speed. It offers one of the fastest pre-approvals in the industry, often within one to two business days, with funding commonly in about two to three weeks. If your timeline is measured in days rather than months, it is the first provider to check.

- Hometap and Point are the reliable middle. Both typically fund in about three weeks, and Hometap is widely regarded as having the most streamlined online application. For most Arizona homeowners, this is the realistic range.

- The appraisal is the real bottleneck, not the provider. Every HEI requires a home valuation, and that step drives the timeline more than the company’s marketing. Responding quickly to document requests is the single biggest thing you control.

In This Article:

- Which HEI Company Funds the Fastest?

- What Does the HEI Funding Timeline Actually Look Like?

- Why Does the Appraisal Slow Everything Down?

- How Can You Speed Up Your Own HEI Funding?

- Is an HEI Faster Than a HELOC or Cash-Out Refinance?

- Why HEIs Skip Income Verification

- Is an HEI Fast Enough for a True Emergency?

- Which Fast HEI Provider Should You Start With?

- Fastest HEI Funding: Common Questions

Which HEI Company Funds the Fastest?

Splitero is the fastest home equity investment provider, offering pre-approval in as little as one to two business days and funding in roughly two to three weeks. Hometap and Point follow at about three weeks. Unlock’s full application-to-funding process tends to run longer, commonly cited at 30 to 60 days, though Unlock wires funds within a few days once you sign your closing documents.

The table below compares funding speed across the major providers as verified in mid-2026. These are typical timelines, not guarantees, and your own appraisal and paperwork can move them in either direction.

HEI Funding Speed by Provider (2026)

| Provider | Pre-Approval Speed | Typical Funding Time | Notes |

|---|---|---|---|

| Splitero | 1 to 2 business days | ~2 to 3 weeks | Fastest overall; simple application |

| Hometap | Fast online estimate | ~3 weeks | Most streamlined digital process |

| Point | Soft-inquiry estimate | ~3 weeks | Funds typically wired after closing |

| Unison | Instant online estimate | Standard timeline | Estimate in seconds, then full underwriting |

| Unlock | Online estimate | ~30 to 60 days | Based locally in Tempe, AZ with in-house underwriters |

The clearest takeaway: if speed is your priority, Splitero is the strongest starting point, with Hometap close behind on the strength of its application experience.

For perspective, an HEI is usually faster than traditional home financing. Industry guides generally place HEI funding at three to six weeks, against roughly 30 to 45 days for a cash-out refinance, because an HEI skips income-based loan underwriting. The trade-off is the appreciation share you give up, not a faster path to cash than every other option.

For the full provider comparison including fees, limits, and Arizona availability, see the Top HEI Companies in Arizona guide.

🐿️ Scout’s Tip

The advertised pre-approval time and the time to actual funding are two different numbers. A one to two day pre-approval still leads into an appraisal and closing that takes weeks. When a provider advertises speed, confirm whether they mean the estimate, the approval, or money in your account.

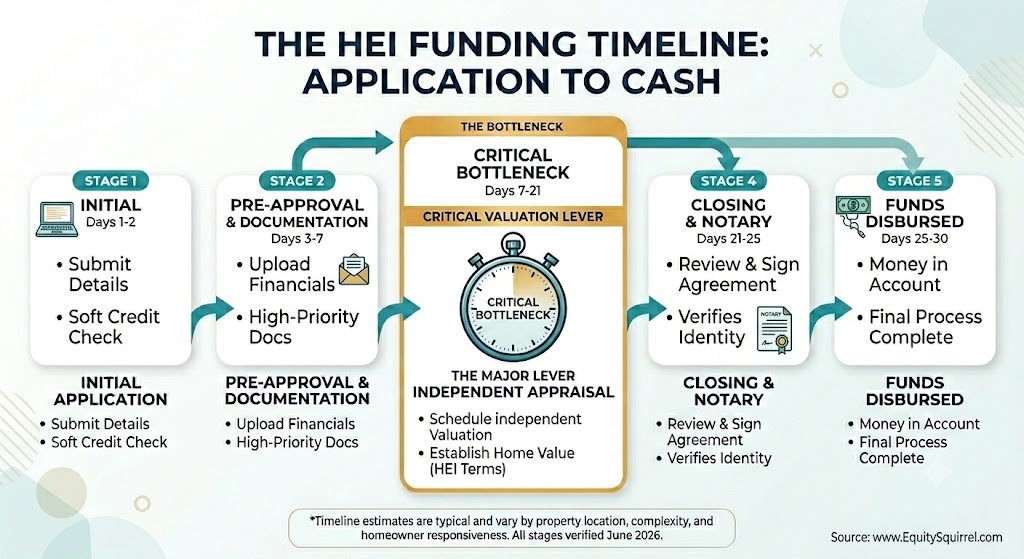

What Does the HEI Funding Timeline Actually Look Like?

A typical HEI funding timeline runs through four stages: a preliminary estimate, a full application, a home appraisal, and closing with funding. From start to finish, most homeowners see funds in two to four weeks, with the appraisal as the most variable step.

Here is what each HEI application stage involves:

Stage 1: Preliminary estimate. You enter your address and basic information and receive a ballpark figure, usually after a soft credit inquiry with no score impact. Formal pre-approvals take 1–2 business days.

Stage 2: Full application and underwriting. You complete the full application, the provider pulls credit, and they order third-party reports. This is where responsiveness matters most.

Stage 3: Home appraisal. An independent appraiser establishes your home’s current value, which sets the starting point for the agreement. This step usually drives the overall timeline.

Stage 4: Closing and funding. Closing often happens with a mobile notary, and funds are typically wired shortly after. This stage is usually quick once the appraisal is complete.

Why Does the Appraisal Slow Everything Down?

The appraisal slows HEI funding because it requires scheduling an independent professional, completing the inspection, and waiting for the written valuation, all on the appraiser’s availability rather than the provider’s. No HEI closes without an established home value, so this step is unavoidable.

The appraisal exists to protect both sides. The provider needs an accurate starting value to calculate their future share, and you benefit from a defensible figure rather than an estimate.

Appraisal timing varies with local demand. In a busy Phoenix-metro market, scheduling can take longer than in a slower period, which is one reason identical applications can fund on different timelines.

🐿️ Scout’s Tip

Have your home ready before the appraiser arrives. Clean, accessible spaces, a list of recent improvements with rough costs, and easy access to every room can prevent a re-visit. A smooth appraisal is one of the few timeline levers you actually control.

How Can You Speed Up Your Own HEI Funding?

You can speed up your HEI funding by preparing your documents in advance, responding to requests the same day, and choosing a provider known for fast processing. The provider’s marketing sets the floor, but your responsiveness sets your real timeline.

Practical steps that shorten the process:

Gather documents before you apply. Have your mortgage statement, homeowner’s insurance, property tax records, and identification ready.

Respond same-day to every request. The single most common cause of delay is a homeowner who takes days to return a signature or a document.

Confirm your provider operates in Arizona before you start, so you do not lose time on an application that cannot close.

Prepare for the appraisal so it can be completed in one visit.

Choose a fast provider if speed is genuinely your priority, rather than defaulting to the most-advertised name.

If you are weighing speed against the size of the payout, see our companion guide on which HEI company has the highest limits.

Is an HEI Faster Than a HELOC or Cash-Out Refinance?

Usually yes. Most HEIs fund in two to four weeks, compared with roughly two to six weeks for many HELOCs and four to eight weeks for many cash-out refinances.

| Product | Typical Funding Timeline |

|---|---|

| Credit Card | Same day |

| Personal Loan | 1–7 days |

| HELOC | 2–6 weeks |

| Home Equity Investment | 2–4 weeks |

| Cash-Out Refinance | 4–8 weeks |

Why HEIs Skip Income Verification

The fundamental reason HEIs skip traditional income verification is that an HEI is not a loan; it is an equity partnership.

When you apply for a traditional mortgage, HELOC, or cash-out refinance, you are taking on debt. Because these products carry mandatory monthly payments, lenders evaluate whether you can repay, generally using your debt-to-income (DTI) ratio and reviewing pay stubs, W-2s, and tax returns. For most closed-end mortgages, including cash-out refinances, federal Ability-to-Repay rules formalize this review.

An HEI completely flips this model:

- No Monthly Payments: Because there is no monthly principal or interest payment due, there is no “ability to repay” a monthly obligation to evaluate.

- Asset-Based Underwriting: Instead of underwriting you (the borrower), the HEI provider underwrites the asset (your home). The investor’s return is tied entirely to the future appreciation or depreciation of the property when you eventually settle the investment (typically via a home sale or refinancing within a 10-to-30-year term).

With a HELOC or cash-out refinance, the lender typically wants:

- Pay stubs

- W-2s

- Tax returns

- Employment verification

- Bank statements

They’re trying to determine whether you can repay a monthly loan payment. As a result, HEIs usually require less income documentation than traditional financing.

Is an HEI Fast Enough for a True Emergency?

An HEI is generally not fast enough for a same-week emergency, because even the quickest providers need roughly two to three weeks to complete an appraisal and close. If you need cash within days, an HEI is rarely the right tool.

For genuinely urgent needs, the appraisal requirement is the limiting factor regardless of which provider you choose. An HEI works best when you have a few weeks of runway, not a few days.

If your need is immediate, it is worth comparing all of your fast-access options side by side, including products that can move faster than an HEI. See the Fast Home Equity Options in Arizona guide for a full comparison.

🐿️ Scout’s Tip

If you are facing a real deadline, start the appraisal step as early as possible and ask your provider directly: what is your realistic funding timeline for my Arizona property right now? A provider’s honest answer to that question is more useful than any advertised average.

Which Fast HEI Provider Should You Start With?

Start with Splitero if speed is your top priority, since it offers the fastest pre-approval and one of the quickest funding timelines. If you also value a smooth digital process, Hometap is a strong second choice that typically funds in about three weeks.

A sensible approach when time matters:

- Confirm availability first so you do not waste days on a non-starter.

- Get a preliminary estimate from Splitero and one other provider to compare both speed and offer.

- Schedule the appraisal immediately once you choose, since it is the longest step.

- Stay reachable through closing so nothing waits on you.

Before committing to any provider for speed alone, make sure an HEI is the right product for your situation. See the Home Equity Investment Guide and confirm you understand the settlement obligations at term end.

Fastest HEI Funding: Common Questions

Splitero is widely recognized as the fastest, offering pre-approval in as little as one to two business days and funding in roughly two to three weeks. Hometap and Point typically fund in about three weeks. These are typical timelines and depend on your appraisal and documentation.

Most home equity investments fund in two to four weeks from application to money in your account. The appraisal is usually the longest single step. The fastest providers can pre-approve in one to two business days, but the full process still takes weeks because a home valuation is required.

The HEI appraisal requires scheduling an independent professional, completing an inspection, and waiting for the written valuation, all on the appraiser’s availability. No HEI can close without an established home value, so this step sets the pace for the whole process.

Usually not for a same-week emergency. Even the fastest providers need roughly two to three weeks to appraise and close. If you need cash within days, compare other fast-access options rather than relying on an HEI.

Yes. Gathering your documents in advance, responding to requests the same day, and preparing your home for a single-visit appraisal are the biggest levers you control. Choosing a fast-processing provider helps, but your responsiveness often makes the larger difference.

The major fast HEI providers generally operate in Arizona, but state availability and timelines change over time. Confirm current Arizona availability and your realistic funding timeline directly with each provider before applying.

The average home equity investment funds in approximately three weeks, although timelines can range from two weeks to more than six weeks depending on the provider, appraisal scheduling, title review, and homeowner responsiveness.

Some homeowners report HEI funding in under two weeks, but this is uncommon and usually requires a fast appraisal, complete documentation, and immediate responsiveness throughout the process.

Credit score primarily affects HEI eligibility and offer terms, but extremely low scores can add underwriting review and slow the process.

EquitySquirrel is an educational resource, not a lender, financial advisor, or legal advisor. This content does not constitute financial, legal, or lending advice. Funding timelines are typical estimates verified June 2026 from provider disclosures and third-party reviews, and they vary by appraisal turnaround, documentation, and applicant responsiveness. Provider availability varies by state. Confirm all current terms and timelines directly with each provider, and consult a licensed financial advisor before making major decisions about your home equity. Aleksandra Kadzielawski, Lic #SA694336000.